In ninth year of recovery, states’ fiscal and economic prospects perked up

After years of slow progress, states benefited from a more promising economic and fiscal environment in 2018. Pressure on state finances eased somewhat as the second-longest economic recovery gained momentum and state tax revenue jumped, at least temporarily. Still, not all states have fully recovered from the shocks of the Great Recession more than a decade ago. Some are in a stronger position than others as they gauge how long the recovery will last.

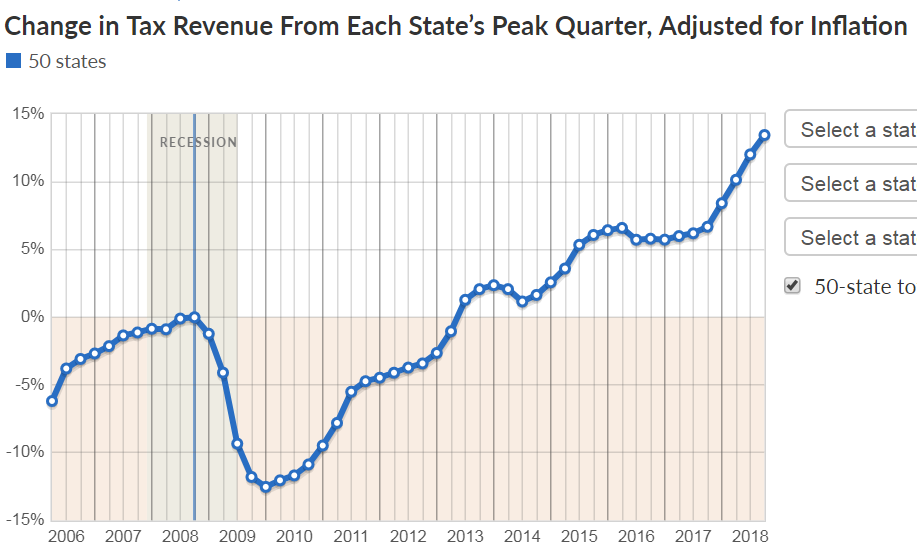

A surge in tax receipts provided budget relief for many states, though some of the extra money was due to short-lived effects from the federal Tax Cuts and Jobs Act. Tax collections in 41 states—the most yet—had surpassed their recession-era peaks by late 2018, after adjusting for inflation. The extra revenue led a number of states to add to their rainy day funds, which could cover a bigger share of spending than before the recession in at least half the states.

Economically, employment rates and growth are on the upswing. Still, the estimated share of prime working-age adults with jobs was lower than before the recession in most states at the end of 2017, and growth measured by state personal income still lagged historic rates.

- Tax revenue. The strongest stretch of tax revenue growth in seven years extended into the third quarter of 2018, but at least some of the gains were temporary and are expected to fade in upcoming quarters. Overall, just nine states took in less tax revenue than before receipts plunged in the downturn, after accounting for inflation. State by state, the recovery has been uneven because of differences in economic conditions and tax policy choices. States with below-peak tax revenue still have less purchasing power than a decade earlier.

- Reserves and balances. States had more savings set aside at the end of fiscal 2018 to weather the next economic downturn than at any point since the 2007-09 recession. Nationwide, rainy day funds held a record amount of money, and at least 26 states’ savings exceeded pre-recession levels when measured as a share of operating costs. A tax revenue surge in fiscal 2018 helped 32 states expand their rainy day funds. Still, just over half of states were less financially equipped, counting rainy day funds plus leftover general fund dollars, to cover their costs than just before the recession.

- Employment-to-population ratio. The U.S. employment rate for adults of prime working age rose in 2017 for a seventh consecutive year, though no state could boast that its core labor pool had clearly surpassed its pre-recession employment rate. The share of prime-working-age adults (ages 25 to 54) with a job clearly remained below pre-recession levels nationally and in 10 states. Employment rates for this population were lower than in 2007 in another 30 states and higher in 10, but not by statistically significant amounts, so the results were inconclusive.

- State personal income. The second-longest U.S. economic recovery has played out unevenly across states. Growth has been strongest in North Dakota and a group of Western and Southern states and weakest in Connecticut and Mississippi, as measured by the rate of change in each state’s total personal income since the start of the Great Recession. State personal income growth—a measure of the economy—has trailed its historical pace. But in a sign of underlying economic strength, gains were widespread among states in the fourth quarter of 2018 from a year earlier.