Key Findings

As technological breakthroughs rapidly shift the frontier between the work tasks performed by humans and those performed by machines and algorithms, global labor markets are undergoing major transformations. These transformations, if managed wisely, could lead to a new age of good work, good jobs and improved quality of life for all, but if managed poorly, pose the risk of widening skills gaps, greater inequality and broader polarization.

As the Fourth Industrial Revolution unfolds, companies are seeking to harness new and emerging technologies to reach higher levels of efficiency of production and consumption, expand into new markets, and compete on new products for a global consumer base composed increasingly of digital natives. Yet in order to harness the transformative potential of the Fourth Industrial Revolution, business leaders across all industries and regions will increasingly be called upon to formulate a comprehensive workforce strategy ready to meet the challenges of this new era of accelerating change and innovation.

This report finds that as workforce transformations accelerate, the window of opportunity for proactive management of this change is closing fast and business, government and workers must proactively plan and implement a new vision for the global labour market. The report’s key findings include:

- Drivers of change: Four specific technological advances—ubiquitous high-speed mobile internet; artificial intelligence; widespread adoption of big data analytics; and cloud technology—are set to dominate the 2018–2022 period as drivers positively affecting business growth. They are flanked by a range of socio-economic trends driving business opportunities in tandem with the spread of new technologies, such as national economic growth trajectories; expansion of education and the middle classes, in particular in developing economies; and the move towards a greener global economy through advances in new energy technologies.

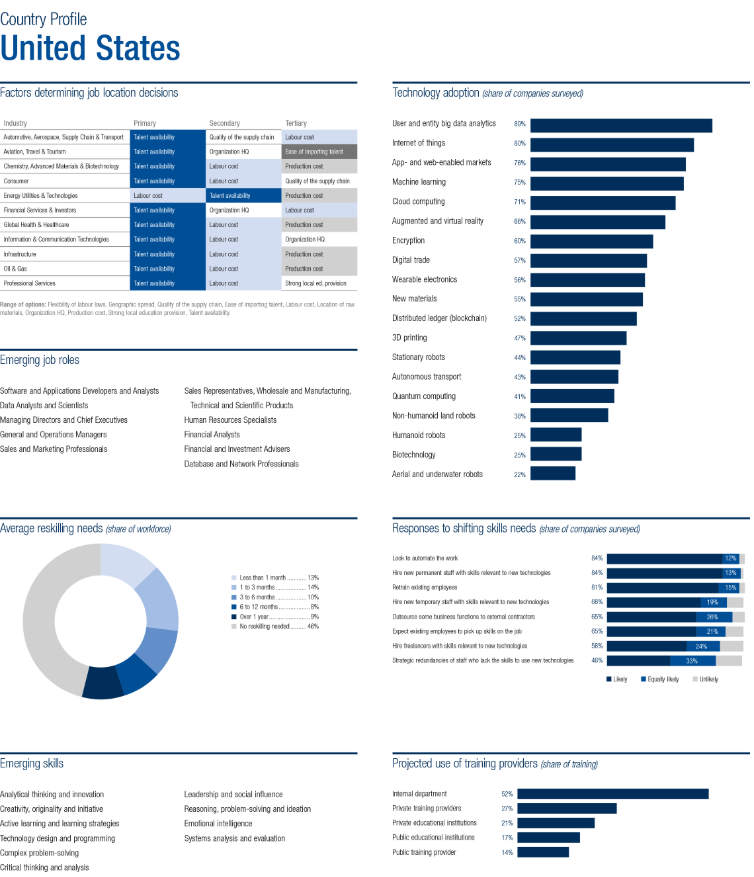

- Accelerated technology adoption: By 2022, according to the stated investment intentions of companies surveyed for this report, 85% of respondents are likely or very likely to have expanded their adoption of user and entity big data analytics. Similarly, large proportions of companies are likely or very likely to have expanded their adoption of technologies such as the internet of things and app- and web-enabled markets, and to make extensive use of cloud computing. Machine learning and augmented and virtual reality are poised to likewise receive considerable business investment.

- Trends in robotization: While estimated use cases for humanoid robots appear to remain somewhat more limited over the 2018–2022 period under consideration in this report, collectively, a broader range of recent robotics technologies at or near commercialization—including stationary robots, non-humanoid land robots and fully automated aerial drones, in addition to machine learning algorithms and artificial intelligence—are attracting significant business interest in adoption. Robot adoption rates diverge significantly across sectors, with 37% to 23% of companies planning this investment, depending on industry. Companies across all sectors are most likely to adopt the use of stationary robots, in contrast to humanoid, aerial or underwater robots, however leaders in the Oil & Gas industry report the same level of demand for stationary and aerial and underwater robots, while employers in the Financial Services industry are most likely to signal the planned adoption of humanoid robots in the period up to 2022.