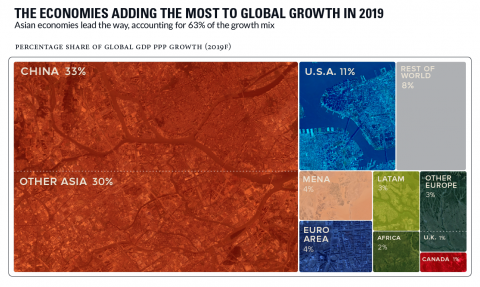

The Economies Adding the Most to Global Growth in 2019

Global economics is effectively a numbers game.

As long as the data adds up to economic expansion on a worldwide level, it’s easy to keep the status quo rolling. Companies can shift resources to the growing segments, and investors can put capital where it can go to work.

At the end of the day, growth cures everything – it’s only when it dries up that things get hairy.

Breaking Down Global Growth in 2019

Today’s chart uses data from Standard Chartered and the IMF to break down where economic growth is happening in 2019 using purchasing power parity (PPP) terms. Further, it also compares the share of the global GDP pie taken by key countries and regions over time.